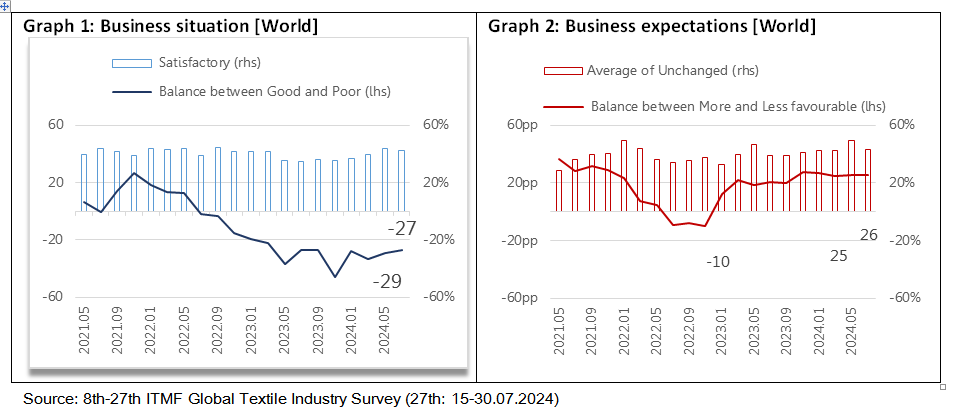

ITMF’s Global Textile Industry Survey (GTIS) in July 2024 reveals that the global textile value chain remains in a very challenging business environment. Even though on average the business situation is dire which reflects a low order intake, business expectations in six months’ time stay positive. This very mixed picture shows that companies are expecting that this unprecedented long duration of a weak business cycle must come to an end eventually.

Order intake has improved slightly in July (-20pp) compared to May (-24pp) and is certainly significantly better than the -50pp in November 2023. Nevertheless, the capacity utilization rate fell slightly from 71% to 68%, the lowest level reached already at the end of 2023. The outlook for both order intake and capacity utilization rate are not indicating a strong improvement.

The major concern in the entire textile value chain was and is weak demand. 66% of participants expressed that they are seeing weak demand as a major concern. That geopolitics is now the second major concern (40%) shows that investors’ and consumers’ sentiments are suffering from wars and geopolitical tensions. High costs remain a challenge too, especially higher logistical costs (24%) due the problems related with the access to both the Suez and Panama Canals but also energy costs (22%) and raw material costs (27%).

Order cancellations are not a major issue as was the case in the immediate aftermath of the Corona-pandemic. Inventory levels are also average and do not pose a major concern for companies along the textile value chain. This was different with retailers and brands that struggled since the end of 2022 with unprecedented inventory levels. In the meantime, they have fallen to a level where it can be expected that they will place more orders again in the coming months.