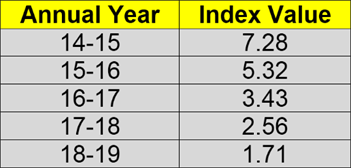

The annual apparel index from CMAI clearly reflects that growth in the sector has been falling continuously for the past five years. The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years.

The annual apparel index from CMAI clearly reflects that growth in the sector has been falling continuously for the past five years. The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years.

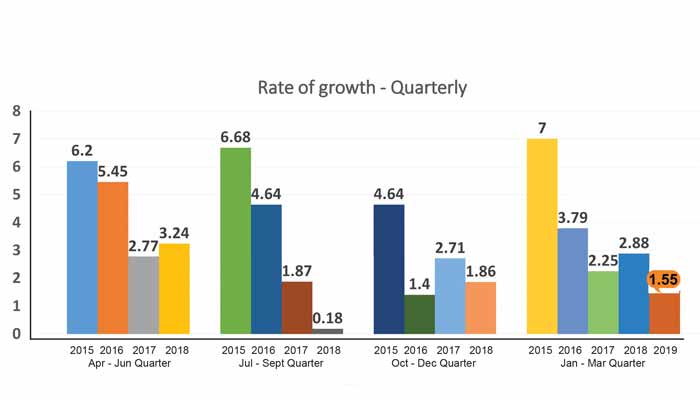

Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points. Similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points. The table clearly shows how the index has been continuously falling over the years. FY2018-19 was marked by low business sentiment even during the festive season, perceived as the best time to make up for turnover losses, as buying is high at that time of the year. Except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18).

When asked about the reasons for the continuous fall in growth rate in the last five years, Rahul Mehta, President, CMAI, said the industry needs to understand the changes in the overall scenario like the change in spending behaviour; earlier people used to save money and spend on their wants, and fashion was one of them, whereas today’s generation has to take care of so many other expenses of rented accommodation and EMIs etc; so the budget available for fashion and apparel buying is going down. Buying behaviour of the youth itself is changing. They are spending far more on electronic gadgets and entertainment. Also, with spending through cash liquidity dropping, impulse buying is impacted. One more important aspect, over the years since the ASP (Average Selling Price) of the most apparel products is dropping; the growth in value seems to be impacted.

When asked about the reasons for the continuous fall in growth rate in the last five years, Rahul Mehta, President, CMAI, said the industry needs to understand the changes in the overall scenario like the change in spending behaviour; earlier people used to save money and spend on their wants, and fashion was one of them, whereas today’s generation has to take care of so many other expenses of rented accommodation and EMIs etc; so the budget available for fashion and apparel buying is going down. Buying behaviour of the youth itself is changing. They are spending far more on electronic gadgets and entertainment. Also, with spending through cash liquidity dropping, impulse buying is impacted. One more important aspect, over the years since the ASP (Average Selling Price) of the most apparel products is dropping; the growth in value seems to be impacted.

Growth dips in Q4 FY 2018-19 too

CMAl’s Q4 Apparel Index touched 1.55 points, a clear reflection of low growth compared to the previous quarter, 1.87.

As earlier, Small Brands sales dipped this quarter, as shown in the table above, and Giant Brands at 5.25 points reported a drop in growth, compared to last quarter’s index figure of 6.00 points. Except Large Brands’ skyrocketing growth from 2.06 points in the previous quarter to 6.93 points in Q4, all other brand groups reported a dip over the last quarter.

While Big brands (Mid, Large and Giant together) have grown at 6.08 points, much more than the 3.52 points of the previous quarter, this is because they have been pushed ahead to reach 6.93 (over three times) from their previous quarter’s 2.06 points. Individually, Small and Mid brands dipped badly, both to 0.63 from their previous quarter index values. Giant brands too have lost growth at 5.25 from 6.00 points previously.

Sales turnover down as inventory holding goes up

If sales turnover were to be considered the only parameter for determining the Apparel Index, this quarter the overall Index would have reflected a growth of 0.52, which is lesser than the previous quarter’s 0.88.

Around 39 per cent brands reported an increase in sales turnover this quarter compared to 48 per cent in the previous quarter. French menswear brand Celio reported positive sales turnover, as Satyen Momaya, CEO, Celio points out. “The increase in sales turnover was due to our quality and we worked on an auto replenish model across our channels.” Similarly, lifestyle brand Monte Carlo gave a positive feedback as Mayank Jain, General Manager, for the brand explained. “The reason for an increase in the sales turnover is we had a strong and good winter. Weather conditions were good and winter lasted for a longer period.” Adds Shitanshu Jhunjhunwala, Director, Turtle, “The increase in sales turnover was due to better work allocation. We had better sizes and availability of these sizes.” Notably the three brands quoted above are from Large & Giant Brands groups.

Almost 25 per cent brands reported a loss in sales turnover compared to 26 per cent in the previous quarter. Except Large and Giant brands, the other two groups this time reported sales losses. Paresh Dedhia, owner, Dare Jeans, explains, “The decrease in sales turnover was mainly due to a slowdown in business in the market post-Diwali. There was a substantial decrease in demand also.” “The reason for the decrease in sales turnover for us was mainly due to closure of our stores,” observes Shyam, President 109° F.

Sell through recorded an Index growth of 1.22 this quarter compared to 0.96 of the previous quarter, still showing pressure on fresh good sales. The maximum growth in sell through was reported by Giant brands. Mid brands, however, clocked in the lowest value of 0.23. Nearly 49 per cent brands reported an improvement in sell through, higher than 46 in Q3. However, sell through decreased for a few. As Shyam revealed, “The reasons for the decrease in sell through is the growing online business which has hampered the offline business up to a point.”

Inventory holding in Q4 is 1.75 points; this is higher than 1.6 points in Q3. Almost 61 per cent respondents across brands said their inventory holding moved north this quarter, higher than 58 per cent in Q3, a very high number and this was responsible for pulling down the overall apparel index value. Increase in inventory holding impacts the overall index negatively. Higher inventory holding indicates more stocks in warehouses or shop shelves. The maximum increase in inventory holding was among Mid brands, causing a low index value; Giant brands on the other hand showed zero change in Inventory holding. Dedhia, Dare Jeans, points out, “Payment cycles have stretched. There is less rotation of funds in the market.”

However, a few brands also managed to decrease their inventory holding. As Deepak Singhla, Marketing Head of Cantabil, says, “The decrease in inventory holding for us was because there was an increase in sales, as store level sales have gone up. Hence, there was no dead stock.” On the same lines, Momaya, Celio, points out, “Inventory holding has actually not increased but has moved. There was more productivity and hence inventory holding has gone down due to replenishment schemes.”

Overall investments are low for the apparel segment this quarter. Fresh investments decreased to nearly 1.56 points, as against 1.62 points last quarter. Nearly 73 per cent respondents reported a rise in investments which is lower than 81 per cent in the previous quarter. The highest investments were done by Mid brands followed by Giant brands.

An average outlook for next quarter

Around 58 per cent (last quarter 52 per cent) brands say the outlook for next quarter is Average. Generally, Q1 of the new fiscal should be better as fresh summer sales pick up and prior to EOSS in July. However, there is no such excitement as the market has still not recovered from the earlier slowdown. Another factor could possibly be the Lok Sabha elections in Q2 this year which may have resulted in expectations of tepid response.